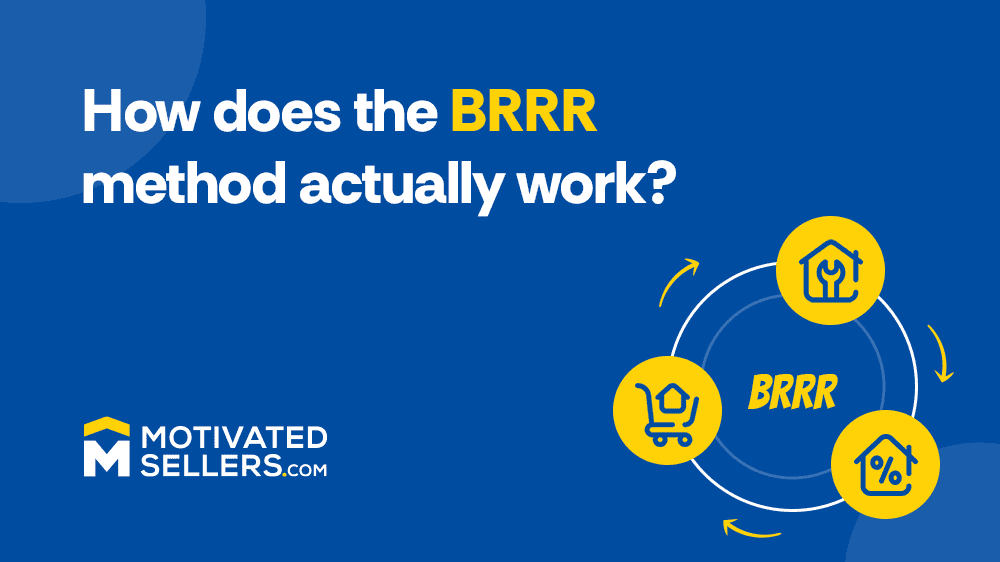

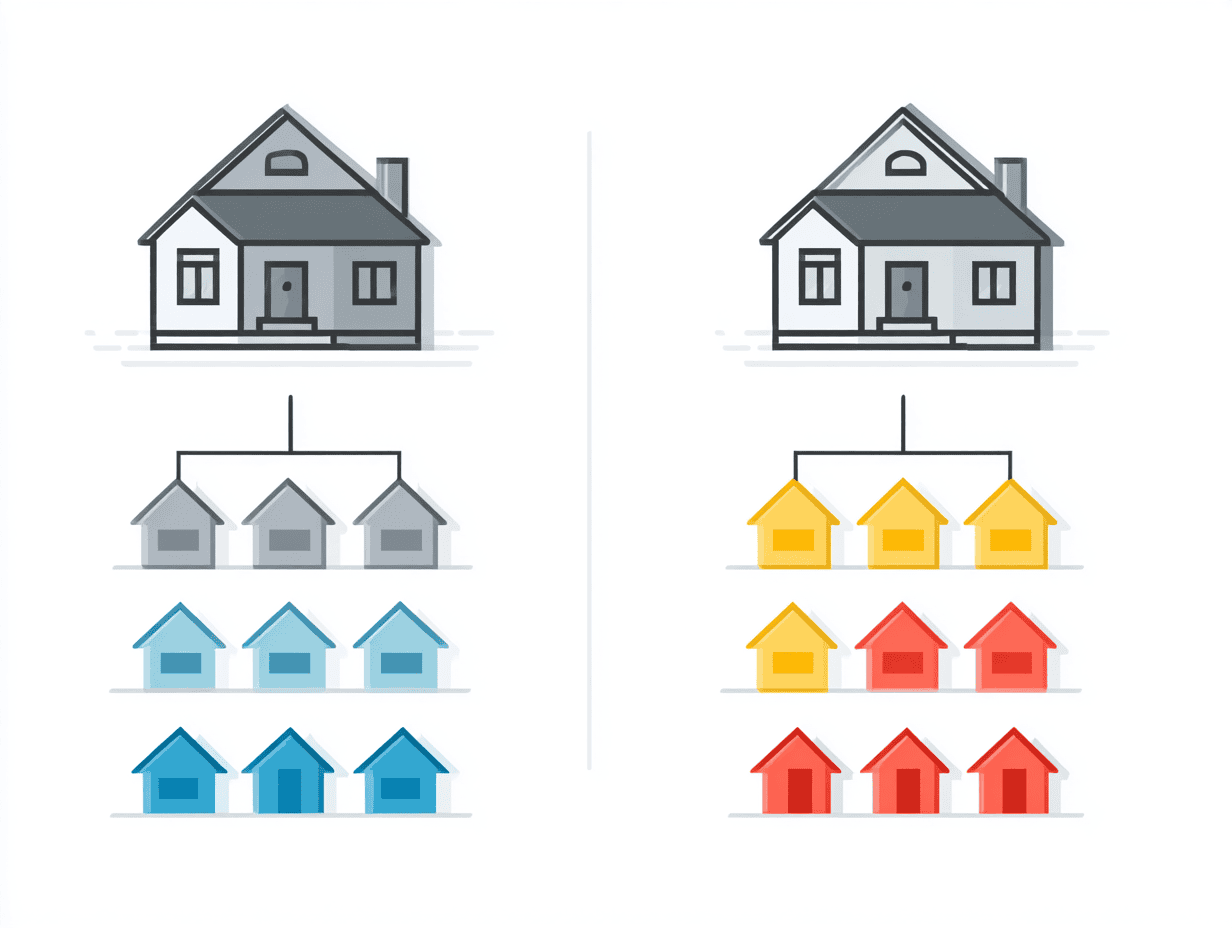

The term “BRRRR method” was first coined and popularized by Brandon Turner of BiggerPockets. It simply refers to the concept of investing in real estate without using your own capital. When you remove the need to invest personal capital, scaling the business becomes easier. Suddenly, you can own 3, 5, or 10 rental properties each year.

In this article, we’ll explore the intricacies of the BRRRR method. The investment community is already familiar with the BRRRR method, but we will go one step further here. After quickly revisiting the definition, we’ll explore:

BRRRR stands for Buy, Rehab, Rent, Refinance, and Repeat.

There are two important investment strategies. You can buy, rehab, and sell, or you can buy and rehab to hold the asset. Both strategies require different planning for successful execution.

For a flip, you’re looking at the expected sales price and your net profit. Let’s say you buy a house for $100k, put $30k into it, and the house sells for $200k. Your net profit after paying all relevant expenses is $55k.

The same property can also be rented for a monthly rent of $1,850. Selling the property is an immediate exit strategy, while the BRRRR method is suitable for building and scaling your rental property portfolio.

The most critical part is to acquire a distressed property at a discounted price. Use a lead generation service like motivatedsellers.com to find an undervalued property. Equity in the property cannot be drawn out of thin air. You will be forcing appreciation via remodeling. So, invest in a property that requires some care, rehab, and you will have equity anywhere between 10% and 30%. (Most important point: use private money or hard money to fund your deal.)

Let’s use our previous example and invest in a property for $100k while putting in rehab work worth $30k. The property now appraises for $200k. That means, after paying for holding costs and interest, you have $55k in equity. For refinancing purposes, you don’t need a down payment, as you have $55,000 in equity, which is more than 25%.

The 70% rule states that you shouldn’t spend more than 70% of the expected appraised value on the purchase and rehab of a property. If the expected value is $200k, then you can spend a maximum of $140k on purchase and repairs. You need the extra buffer to protect against unexpected turns.

This is the most challenging part of the BRRRR method. You need to pull a credit score and qualify for a traditional mortgage. The down payment is not an issue if you bought right. You have equity in the property.

The lender will consider the appraised value of the property. You can borrow up to 80% of the appraised value. So in our example, you can borrow $160,000 from a conventional bank. After paying $150k to your hard money lender, you will still have $10k in your pocket and 20% equity in the property.

Most real estate investors struggle with refinancing because:

Big corporate banks have restrictions, and you won’t be getting money for several deals in a year. Always go to your local community bank or credit union, as they have flexible terms and need investor clients. Build a relationship so you can refinance several properties over the course of the next 12, 24, or 60 months.

It’s a common question asked by many real estate investors. The DTI ratio matters if you are borrowing money to purchase your primary residence. However, it doesn’t matter for the BRRRR method. You are refinancing an income-producing property, and the income from the property will offset the mortgage-related costs. The bank is not going to look at your personal income. They will rather look at the projected rental yield and the property value.

That brings us to another important rule: the 1% rule in real estate.

For a $200k property, the monthly rental yield should be 1% of the total investment, or $2,000. Continue your search if getting a 1% rental rate doesn’t seem realistic in a specific neighborhood.

Research rental rates because your monthly rent must cover occasional vacancies, repairs, and mortgage payments. Ideally, it should be 1% of the property value, but it could be less depending on the area. It could be a trouble down the road if the property doesn’t produce enough cash flow each month.

Your local bank will send a 3rd-party appraiser to get a professional opinion of the market value of your property. The appraisal can be low or high depending on several factors. Here is one thing you should always do:

Prepare a marketing packet that highlights all the improvements you made to the property and your opinion of the market value. Meet the appraiser in person. Answer their questions and tell them how you have improved the property and why you think it’s valued at a certain number.

Doing so creates goodwill, and the appraiser will carefully notice all the improvements. If you don’t meet the appraiser, they might choose a lower number to stay on the safe side. Once you highlight your good work, the chances are that your home will receive more attention. The results can still vary, but this extra step can help your deal.

A property refinance is basically tax-free money. Depreciation, interest deduction, and other tax benefits are available to landlords. Managing several properties can help qualify you as a full-time investor, which has more tax perks. After a decade, if you want to sell a property, you can reinvest the funds using a 1031 exchange.

It’s not an ideal strategy for your first deal. There are lots of moving parts, like:

All of these areas require expertise. New investors can begin by wholesaling, then do rehabs while slowly moving towards the BRRRR method.

It’s a long-term game that’ll continue for the next 10–30 years (depends on your mortgage terms). There will be cash flow, but most of that will go towards mortgage payments and management-related expenses. The benefit is that you will own a portfolio of positive cash flow properties without investing your own money. You’ll have equity, and you’ll own these properties clear and free after 30 years.

Utilizing the BRRRR method requires patience and strategic thinking. Over the next 30 years, you’ll face the volatility of the real estate market. There will be tenants who ruin the property. On certain occasions, banks will refuse loans, and other issues will happen. However, the effort is worth the reward. No one said that investing in real estate is easy, but financial rewards await those who put in the effort.

Buy, rehab, rent, and refinance—This strategy suggests that you are in the game for the long term. Market conditions can change. A recession can happen, potentially affecting the value of your properties. There is a risk of not finding a conventional loan to refinance your property. These types of risks are inherently present in all real estate transactions. That’s why it’s important to keep a safety cushion in all situations. Invest in undervalued assets so you will always have equity, no matter what. Stay persistent and look at the long-term goal. Even with a recession, property values will bounce back. You cannot control everything, but investing through the BRRRR method is an opportunity to multiply your investment capabilities.

Consider the needs of potential tenants when rehabbing a property. Choose durable materials and low-maintenance fixtures. Select neutral designs and establish a hallmark design across your rental properties. Doing so will slowly build your brand.

A beautifully renovated house will attract tenants. Choose a property manager who can assist with tenant screening, onboarding, and continuous management of rental properties.

You can acquire a primary residence with just a 3.5% down payment and a minimum credit score. You don’t have to go through all the trouble of rehabbing distressed assets and refinancing them. The BRRRR method is not suitable for primary residences because you cannot immediately rent them. And it’s not wise to use a hard money loan for extended periods because of the high interest rate. Ideally, you want to refinance properties after rehab and move your money out as soon as possible.

Ideally, yes. You will either start with hard money or private money. Conventional loans are not used to close deals for distressed properties because of time limitations. You need a lot of cash without strict credit requirements, and you need cash quickly. It’s best to build your relationships and acquire private money at favorable rates.

Once the renovated property is rented, you can refinance. At that time, you will use a conventional loan. There can be a seasoning period of 3–12 months when you need to own the property before a lender will approve your refinancing application. Most investors will own the distressed property for 3–6 months (counting time for improvement and finding tenants) before refinancing. However, if you have built relationships with the local bank, you can refinance homes quickly without having to wait for several months.

Real estate investors with excellent credit scores buy, rehab, and refinance multiple properties each year. Your credit score can take a small hit (1–3 points) for each credit check, but you can offset that by timely payments of other debts. Each payment also boosts your score. Successful real estate investors shop for multiple lenders in 30 days because multiple credit checks are counted as one in a grace period of 30–60 days. And it’s crucial to continue paying your debt by selecting top tenants.

Once you have this setup, you’ll be ready to BRRRR your next property and then another one. Have questions about the BRRRR method? Drop a comment and we’ll answer it for you.

Success in real estate starts with the right leads. At MotivatedSellers.com, we provide the quality and consistency you need to close more deals.

Motivated sellers are looking for investors like you!

Contact us at

MotivatedSellers.com is committed to digital accessibility for individuals with disabilities. We welcome feedback and accommodation requests. If you need assistance or wish to report an issue, please contact us.

Motivated Sellers is a registered trademark of Seliger Ideas Inc. and is not affiliated with MotivatedLeads.com

Copyright © 2026 Seliger Ideas Inc. All Rights Reserved.